The 2026-27 Budget, explained

What the 12 May 2026 Budget changed for property investors

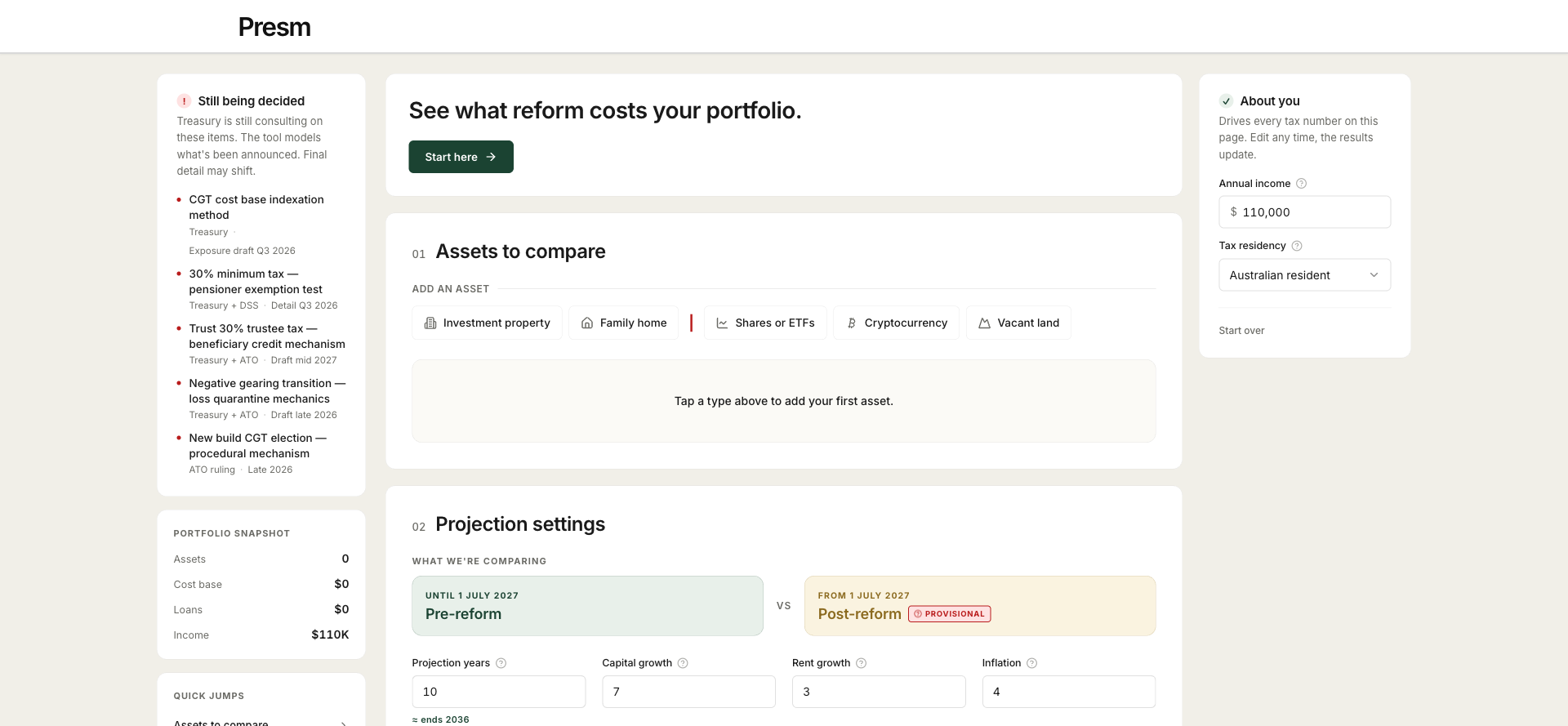

On 12 May 2026 the Treasurer handed down the 2026-27 Federal Budget. Three measures inside the tax reform chapter directly affect Australian property investors. None of them are law yet. All three are scheduled to commence on 1 July 2027 if the legislation passes, and each carries grandfathering rules for property already held before that date. This page summarises what was announced, who it hits, who is protected, and how to model the dollar impact on your specific portfolio.

CGT reform: from a 50% discount to indexation plus a 30% minimum effective tax

The current rule is straightforward. Hold an investment property for more than 12 months, sell it, and you discount the capital gain by 50% before adding it to your taxable income. A $400,000 gain becomes a $200,000 inclusion taxed at your marginal rate. For a 47% marginal earner, that is roughly $94,000 of tax on a $400,000 gain.

The announced replacement has two moving parts. First, the cost base of the asset is uplifted by inflation across the holding period using an indexation factor. The taxable gain is the sale proceeds minus the inflation-adjusted cost base, which is normally smaller than the headline gain. Second, a 30% minimum effective tax is applied to the inflation-adjusted gain. The practical result is that very long holds in low-inflation periods can fare better under indexation than the discount method, while shorter holds in high-inflation periods may end up worse.

The Presm Wealth Accelerator models the long-run after-tax outcome on portfolio scenarios under both regimes. The Tax Reform Lens calculator above does the same on a single property purchase decision.

Negative gearing: new builds only from 1 July 2027

Today, an investor whose rental income falls short of holding costs (interest, rates, insurance, depreciation, repairs) can deduct the net loss against their salary at their marginal tax rate. This deduction is one of the most discussed features of Australian property investment.

From 1 July 2027 the Government has announced that negative gearing on established dwellings will be removed for new acquisitions. Newly built dwellings, defined as never previously occupied, will retain access to negative gearing as before. The policy intent is to channel investor capital toward expanding housing supply rather than recycling existing stock.

For investors holding established properties on or before 30 June 2027, the rules are unchanged for the life of that ownership. Settlement after 1 July 2027 on an established dwelling falls under the new regime. The decision for many investors becomes one of timing and asset type, not whether to invest at all.

Grandfathering: what existing investors keep

The grandfathering provisions are the most important detail in the announcement and the most often missed in headlines. As published, every property held by an investor on 30 June 2027 continues under the current rules for the full duration of that ownership. That means:

- The 50% CGT discount continues to apply on sale of any pre-cutoff property held for more than 12 months.

- Net rental losses on pre-cutoff properties continue to be deductible against other income at your marginal rate.

- Existing trust distributions of pre-cutoff income continue under current trust tax rules.

The cost-of-capital effect of the reform is therefore much smaller for an investor with an existing portfolio than the headline reads. Modelling matters here. Buying a final pre-1 July 2027 property to lock in grandfathering is a defensible strategy if the asset stacks up; it is not a strategy if the asset does not.

Trust 30% minimum tax

Discretionary and family trusts have long allowed an investor to stream income to lower-rate beneficiaries: a spouse not working, an adult child at university, a parent on the pension. The marginal rate on streamed income could fall below 19% in some cases.

The new 30% minimum tax sets a floor. Trust distributions of income and capital gains from 1 July 2027 onwards will attract an effective tax rate of at least 30% in the hands of the beneficiary. Existing structures are not unwound. Income earned before 1 July 2027 continues under current rules. Distributions of pre-cutoff retained earnings also retain current treatment.

The change has the largest impact on portfolios that were relying on rate-streaming as a structural benefit. The Presm Entity Land Tax Simulator and the SMSF Tax Calculator compare ownership structures across personal, joint, trust, company, and SMSF, modelling the effect of the new floor on total after-tax position.

How Tax Reform Lens models the dollar impact

The calculator above takes the property purchase you are considering, your marginal rate, your holding period, and your growth and rental assumptions, then runs the after-tax outcome under both the current law and the announced reform. Side by side. The output is a single number for each scenario plus the year-by-year cashflow trail behind it, so you can see exactly when the reform bites and how the grandfathering window changes the answer.

Run your numbers in the calculator. No signup, no email. Modelled on the announced rules; not advice.

Frequently asked questions

On the announced 2026-27 Federal Budget property tax reforms. Subject to legislation.

- What did the 2026-27 Federal Budget actually change for property investors?

- The 12 May 2026 Budget announced three major property tax measures: replacing the 50% CGT discount with an indexation method paired with a 30% minimum effective tax on capital gains; restricting negative gearing to newly built dwellings for purchases settled on or after 1 July 2027; and a 30% minimum tax on trust distributions to wash out the headline rate gap between trusts and individuals. All three are reforms, not yet legislation, and each carries its own grandfathering treatment for property held before commencement.

- When do the new rules take effect?

- The announced commencement date is 1 July 2027 for both the negative gearing change and the new CGT regime. The trust minimum tax measure aligns with the same start date. The Government has flagged a draft legislation period of around 12 months, with passage expected in the first half of 2027. None of the rules apply to the current 2025-26 financial year.

- Will the changes apply to property I already own?

- Per the announcement, existing properties as at 30 June 2027 are grandfathered for both negative gearing deductibility and the CGT discount method. You keep the 50% CGT discount and the ability to negatively gear those properties under the current rules for the life of your ownership. New purchases settled on or after 1 July 2027 fall under the new regime.

- How does indexation work compared to the 50% discount?

- Indexation lets you uplift the cost base of an asset by inflation over the holding period. The taxable gain is the sale proceeds minus the inflation-adjusted cost base, which can be smaller than the headline gain. The 30% minimum effective tax is then applied to that adjusted gain. For long-held assets in low-inflation periods, the 50% discount usually beats indexation. For shorter holds or higher-inflation periods, indexation can sometimes win. Tax Reform Lens runs both calculations on your specific holding period and inflation assumptions.

- Can I still negatively gear an existing investment property after 1 July 2027?

- Yes. Properties held before 1 July 2027 retain access to negative gearing under the current rules. You can continue to deduct net rental losses against your other income at your marginal tax rate. The restriction only bites on new acquisitions of established dwellings settling on or after that date. Newly built dwellings remain negatively geared regardless of settlement date.

- What does the 30% minimum tax on trusts mean?

- Trust beneficiaries currently pay tax at their marginal rate on distributions, which can be as low as 0% for a beneficiary below the tax-free threshold. The new measure imposes a 30% minimum effective tax on income and capital gains distributed by family and discretionary trusts. The intent is to remove the rate-arbitrage benefit of streaming distributions to low-income family members. Existing structures keep current rules for income earned before 1 July 2027.

- Should I bring forward a property purchase before 1 July 2027?

- Possibly, but only after running the numbers. Buying purely to pre-empt a tax change is not a strategy. Buying because the property stacks up on its fundamentals AND the grandfathering preserves the deduction is a strategy. Tax Reform Lens compares the after-tax position of buying now under current law against buying after 1 July 2027 under the new regime, holding all property assumptions equal. If the tax delta is large relative to the change in market timing risk, that is a signal to act. If it is small, it is not.

- How does the reform affect SMSF property investment?

- SMSFs already pay 15% on rental income and 10% effective CGT (after the one-third discount) in accumulation phase. The new CGT method does not apply to super funds in the same way as individuals, so the SMSF cost base treatment broadly continues. The Presm SMSF Tax Calculator runs SMSF versus personal scenarios under both current and announced rules, so you can see whether the reform widens or narrows the gap.

- Where can I see the official text of the announcement?

- The Treasury 2026-27 Budget papers are published at budget.gov.au, with the property and tax reform measures grouped in the tax reform chapter. Accountants and law firms have published detailed summaries during the post-Budget consultation period. Always check current Treasury and ATO guidance before making a binding decision; this page is informational, not personal tax advice.

- Is Tax Reform Lens advice?

- No. Tax Reform Lens is a modelling tool that quantifies the dollar impact of the announced reforms on a specific portfolio you describe. It does not consider your full personal situation, does not constitute tax or financial advice, and its outputs depend on the inputs you provide. For decisions on real money, work with a registered tax agent and a licensed financial adviser.